|

Subscribe / Renew |

|

|

Contact Us |

|

| ► Subscribe to our Free Weekly Newsletter | |

Construction Bids

| home | Welcome, sign in or click here to subscribe. | login |

| |

May 8, 2026

Hattenburg

|

Day

|

Brandon

|

Effective April 1, 2026, the gross income of self-storage facilities located in Washington state is subject to business and occupation (B&O) tax. B&O tax is generally paid quarterly, with the first payment due by July 25, 2026. Self-storage facilities also no longer qualify for Active Non-Reporting (ANR) status if their annual gross income exceeds $125,000.

UNDERSTANDING THE NEW LAW

RCW 82.04.290 requires that certain businesses pay Washington's B&O tax on their gross income. Prior to April 1, 2026, the rental income derived from self-storage facilities was considered rental of real estate and therefore not subject to B&O tax.

The new law (Engrossed Senate Substitute Bill (ESSB) 5794) specifically changed this treatment by adding the business of renting or leasing individual storage space at “self-service storage facilities” to the class of business activity that must pay B&O tax under RCW 82.04.290(4).

RCW 19.150.010(10) defines self-service storage facilities as “any real property designed and used for the purpose of renting or leasing individual storage space to occupants who are to have access to the space for the purpose of storing and removing personal property on a self-service basis.”

As a result, self-storage operators and owners must now pay B&O tax on their gross revenue quarterly starting Q2 2026. In passing ESSB 5794, the Legislature cited its interest in having a balanced tax system and modified existing exemptions in furtherance of its public policy interests.

B&O TAX

Washington's B&O tax on gross income applies regardless of whether a business operates at a profit or loss. The B&O tax base is not reduced by deductions for labor, materials, taxes, or other business costs.

B&O tax is generally paid quarterly, with the first deadline for self-storage facilities set for July 25, 2026. B&O tax returns must be filed online through Washington's Department of Revenue's MyDOR system.

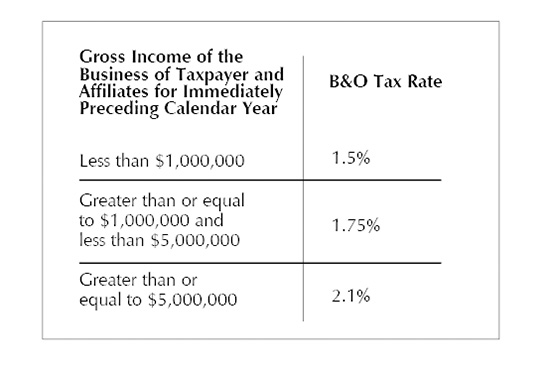

The applicable B&O tax rate is based on the aggregate gross income of the business subject to tax for the taxpayer and its affiliates for the immediately preceding year. The B&O tax is calculated by multiplying the business's gross income by the following applicable tax rates.

ACTIVE NON-REPORTING (ANR) STATUS

In addition to paying the B&O tax, self-storage facilities with annual income exceeding $125,000 no longer qualify for ANR status, even if they do not engage in retail sales (i.e., selling moving supplies). Operators and owners previously on ANR status should confirm whether their income levels require an update to their ANR filing status.

LOOKING AHEAD

The passage of ESSB 5794 confirms the Washington State Legislature's focus on supporting public institutions through increasing taxes on businesses. The bill explicitly characterizes parts of the existing tax code as being protective of private interests and expresses the Legislature's intent to create a balanced tax system.

The Washington Self-Storage Association (WSSA) believes that the B&O tax applied to self-storage facilities raises Washington state constitutional concerns, asserting the tax unfairly targets the self-storage business. WSSA suggests that excluding self-storage rental income from the definition of real estate income violates the uniformity clause of Washington's Constitution by taxing only a portion of real estate income, while excluding rental income from office, industrial, retail, and multi-family properties. Litigation challenging the new law is thus likely to happen in the near future.

Adam Hattenburg and Cailin Day practice in the Real Estate group at Stoel Rives LLP, and may be reached at adam.hattenburg@stoel.com and cailin.day@stoel.com. David Brandon is a member of the firm's Corporate group and handles domestic and international tax matters. He may be reached at david.brandon@stoel.com.